AUTHOR’S NOTE: Most Filipinos think of Meralco as the electric company. The monopoly. The entity you cannot leave. That is true, and it is also increasingly incomplete. Under its current owners, Meralco has been quietly — and methodically — building an energy business that now extends well beyond the wires.

This is the second of 2 pieces on Meralco. The first piece covers the ownership history. This one covers what the company has become: why its distribution business now accounts for less than half of its profits, what it has been building in its place, and what a rate increase currently before the government regulator means for every Filipino who pays that monthly bill.

My 2-part series on Meralco:

Part 1: The long, complicated life of Meralco

Part 2: From delivery driver to factory owner: How Meralco rewrote its own rules

Ask most Filipinos what Meralco is and they will say the same thing: it is the electric company. The monopoly. The reason your electricity bill is so high. The company you cannot leave even if you wanted to, because there is no alternative in Metro Manila and the surrounding provinces. All of that is true, and none of it is wrong. But it is increasingly incomplete as a description of what Meralco actually is today.

I recently attended a corporate briefing organized by BPI and featuring Paul Jayson Ramos, Meralco’s investor relations executive, who spent about an hour and a half walking a room of investors and analysts through what the company has become and what it intends to build. The numbers he presented tell a story that most Meralco customers, the 8.2 million households and businesses that pay that monthly bill, have no particular reason to know about, because it lives in the language of earnings reports and megawatts rather than electricity bills.

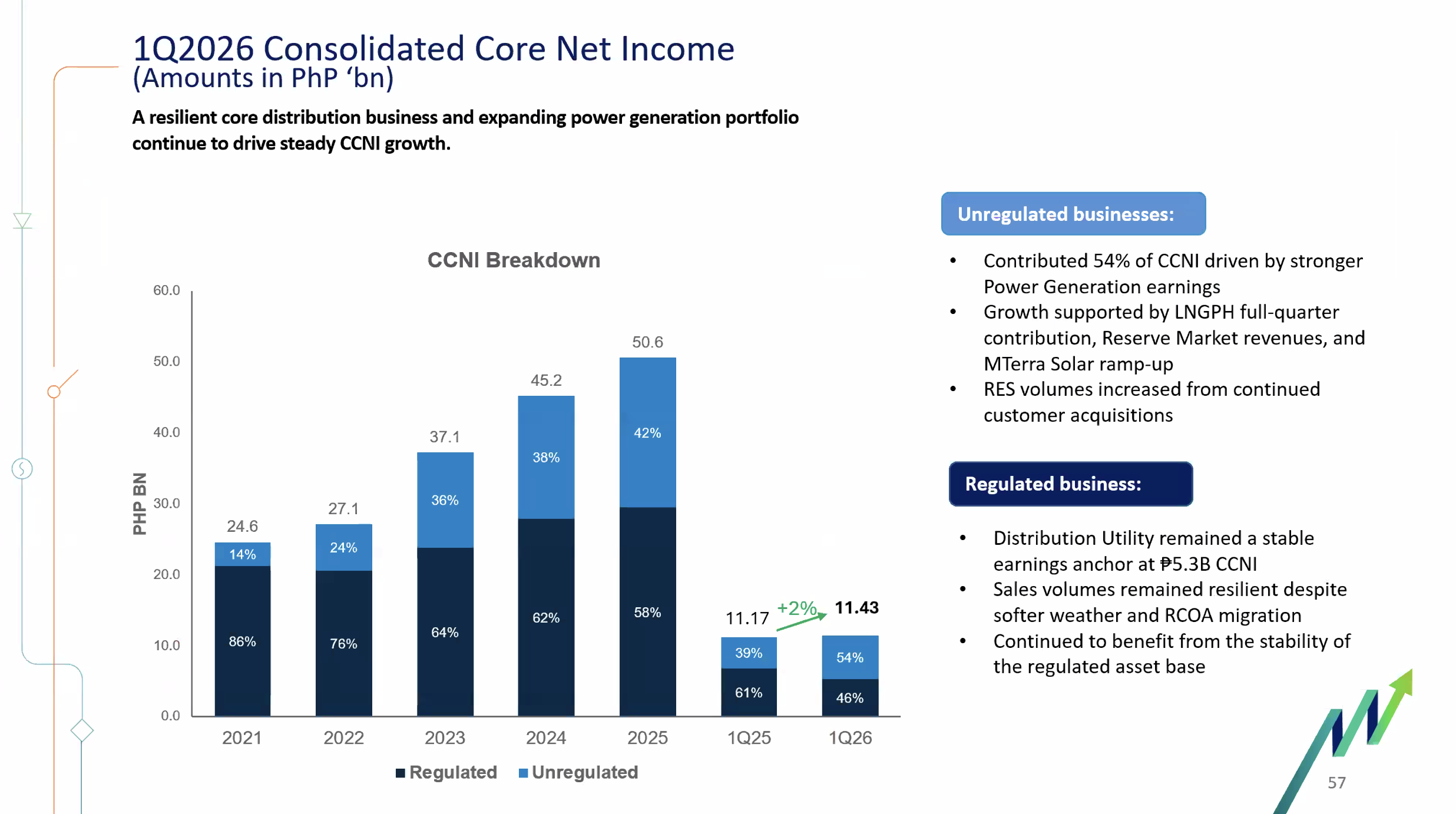

In 2021, the regulated distribution business, the poles, wires, and transformers that carry electricity from the national grid into Filipino homes and offices, contributed 86% of Meralco’s total profits. It was, by any measure, the entire company. Everything else was a rounding error.

By the first quarter of 2026, that same business contributed 46%. And the company had not shrunk. It had more than doubled its earnings over those 5 years. What happened in between is the story of how a regulated utility, theoretically boxed in by a government-approved ceiling on what it can earn, built an entirely new company around its original one, and then kept building until the new company was almost as large as the old one and growing considerably faster.

This is the second piece in a 2-part series on Meralco. The first covered how the company came to be and who has owned it across 122 years. This one covers what it has become.

Why the distribution business has a built-in ceiling

To understand why Meralco built beyond distribution, you first have to understand what distribution actually earns and what it does not.

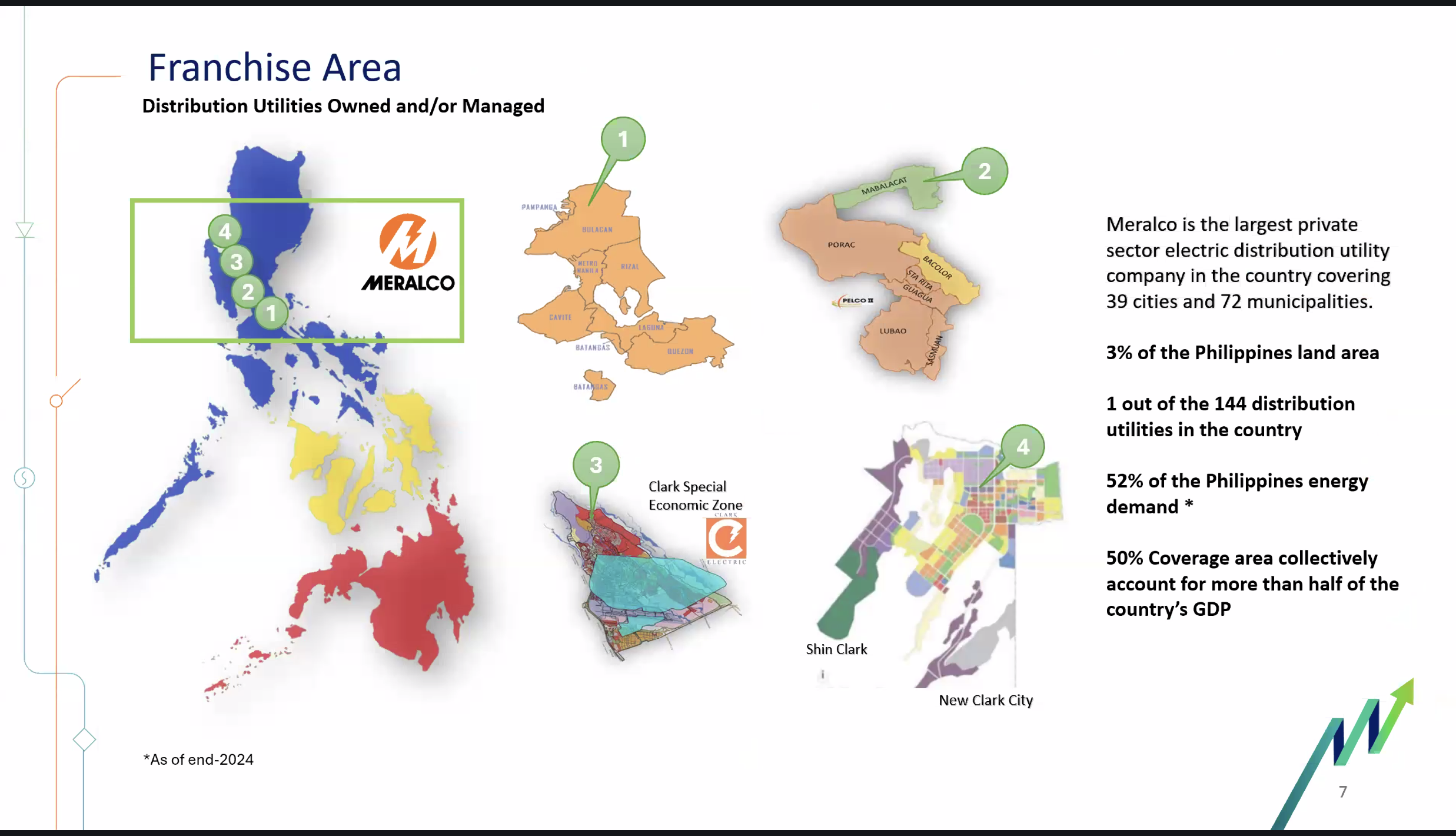

Meralco is the only company allowed to deliver electricity across Metro Manila and the surrounding provinces. That exclusivity sounds like an extraordinary advantage, and in some ways it is. But it comes with a condition that shapes everything: the government, through the Energy Regulatory Commission or ERC, sets the maximum amount Meralco can charge per kilowatt-hour for the service of delivering electricity. Every 4 years, there is a formal process called a rate reset, where Meralco files for a new distribution rate, the regulator reviews it, and a number is set. Until the next reset, that is the ceiling. Meralco cannot earn more than what the ERC approves, no matter how many customers it adds or how much electricity flows through its wires.

Think of it this way: Meralco owns the only road into a very large town, but the government gets to decide what the toll should be. The customers are guaranteed. The income is not.

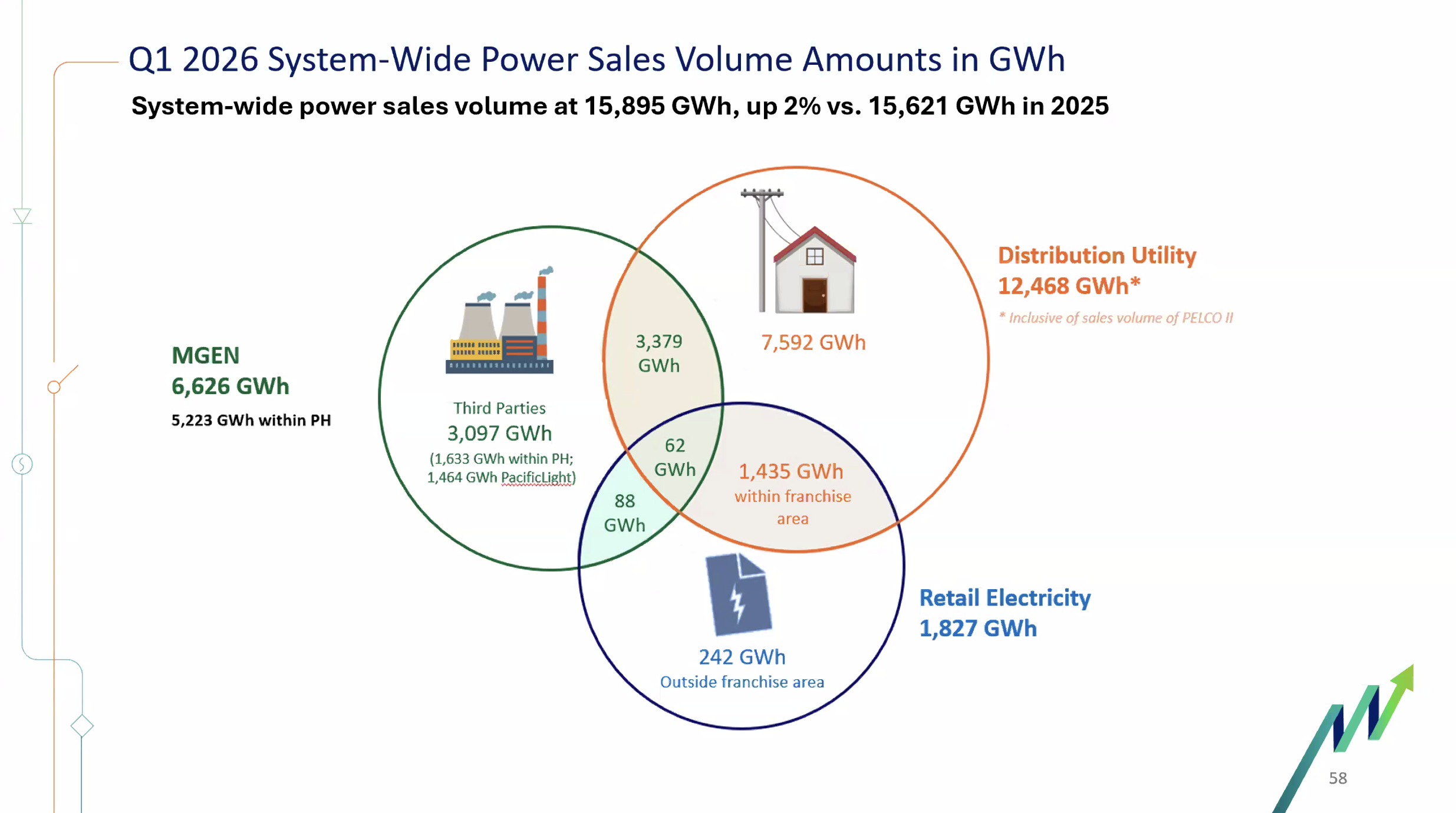

There is a 2nd constraint that makes the first one feel even tighter. When you pay your Meralco bill, most of the money you hand over does not stay with Meralco. The largest portion, often more than half the total bill, is the generation charge, the cost of the actual electricity produced by the power plants that supply the grid. Meralco collects this from you and forwards it directly to those power plants. It keeps none of it. The generation charge comprises roughly 52% of a typical monthly bill, and Meralco’s actual earnings come only from the distribution charge, the transmission pass-through, and related fees, which are the smaller slices of what you pay.

For a company that processes over P450 billion in annual revenues, roughly 78% of that money belongs to someone else. Meralco is, in large part, a collection agency on behalf of power plants and the transmission network.

Given that reality, the distribution business grew in the years after the 2001 EPIRA law mostly through 2 mechanisms: more customers connecting to the grid as Metro Manila expanded, and more electricity being consumed as the economy grew. Both produced real revenue. But both were inherently slow, incremental, and capped at the edges by geography, by the regulatory formula, and by the fact that distribution rates had not been meaningfully adjusted in well over a decade. From 2021 to early 2026, the distribution rate that customers paid barely moved, even as Meralco’s infrastructure spending climbed steeply.

This was the underlying pressure. The only way to grow meaningfully, to earn returns that matched the scale and risk of running the most important piece of infrastructure in the country’s economic heartland, was to build beyond the wires. And that is exactly what Meralco did, methodically and at scale, under the ownership coalition led by Manuel V. Pangilinan and the Gokongwei family.

The strategy: build around the monopoly, not just inside it

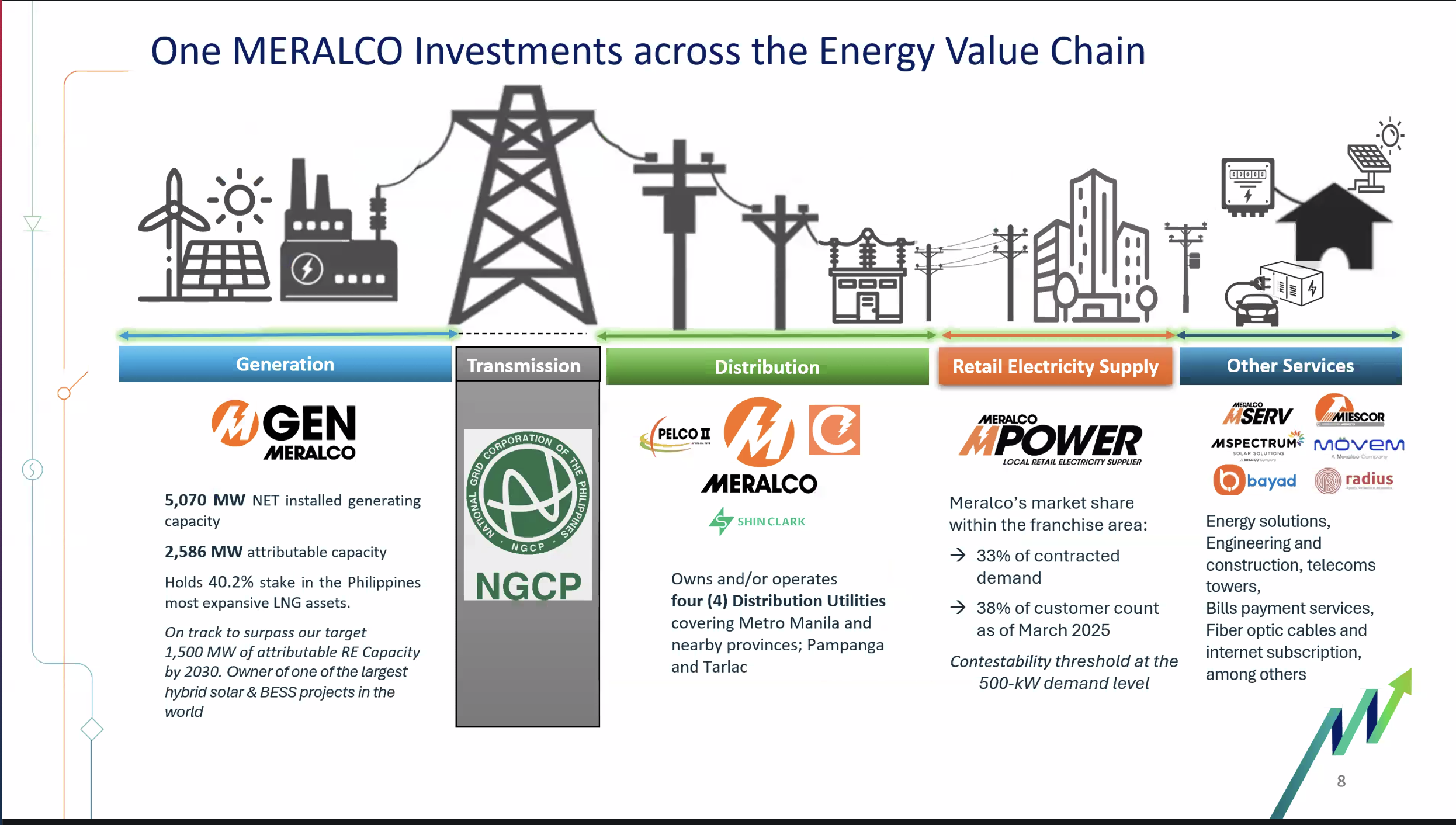

The EPIRA law that restructured the Philippine electricity industry in 2001 was designed to prevent any single company from controlling the entire supply chain from power plant to wall socket. It split the industry into 4 layers, generation, transmission, distribution, and retail supply, and assigned Meralco firmly to the distribution lane.

But EPIRA also left a door open. It allowed distribution companies to source up to 50% of their electricity supply from plants they owned or controlled. That provision, written as a limit on self-dealing rather than as an invitation to expand, turned out to be the crack through which Meralco’s entire transformation would eventually pass.

The strategy that took shape under the Pangilinan-Gokongwei leadership was not a single dramatic pivot. It was a deliberate, multi-year accumulation of businesses in the parts of the electricity value chain that EPIRA either permitted or did not restrict. Generation was one lane. Retail supply to large commercial customers was another. Rooftop solar was a third. Digital infrastructure, payment services, and fiber internet were adjacent bets. Each subsidiary was technically separate. Each competed in its own market. But they all fed from the same anchor, the distribution franchise that guaranteed Meralco a captive relationship with 8.2 million customers across the Philippines’ most economically dense territory.

The financial result of that strategy is visible in a single line from Meralco’s investor presentations: the share of unregulated business in the company’s total profits grew from 14% in 2021 to 54% in the first quarter of 2026. The regulated wires business went from being virtually everything to being less than half, not because it declined, but because the rest of the company grew around it and eventually past it.

The generation business: from coal to LNG to solar

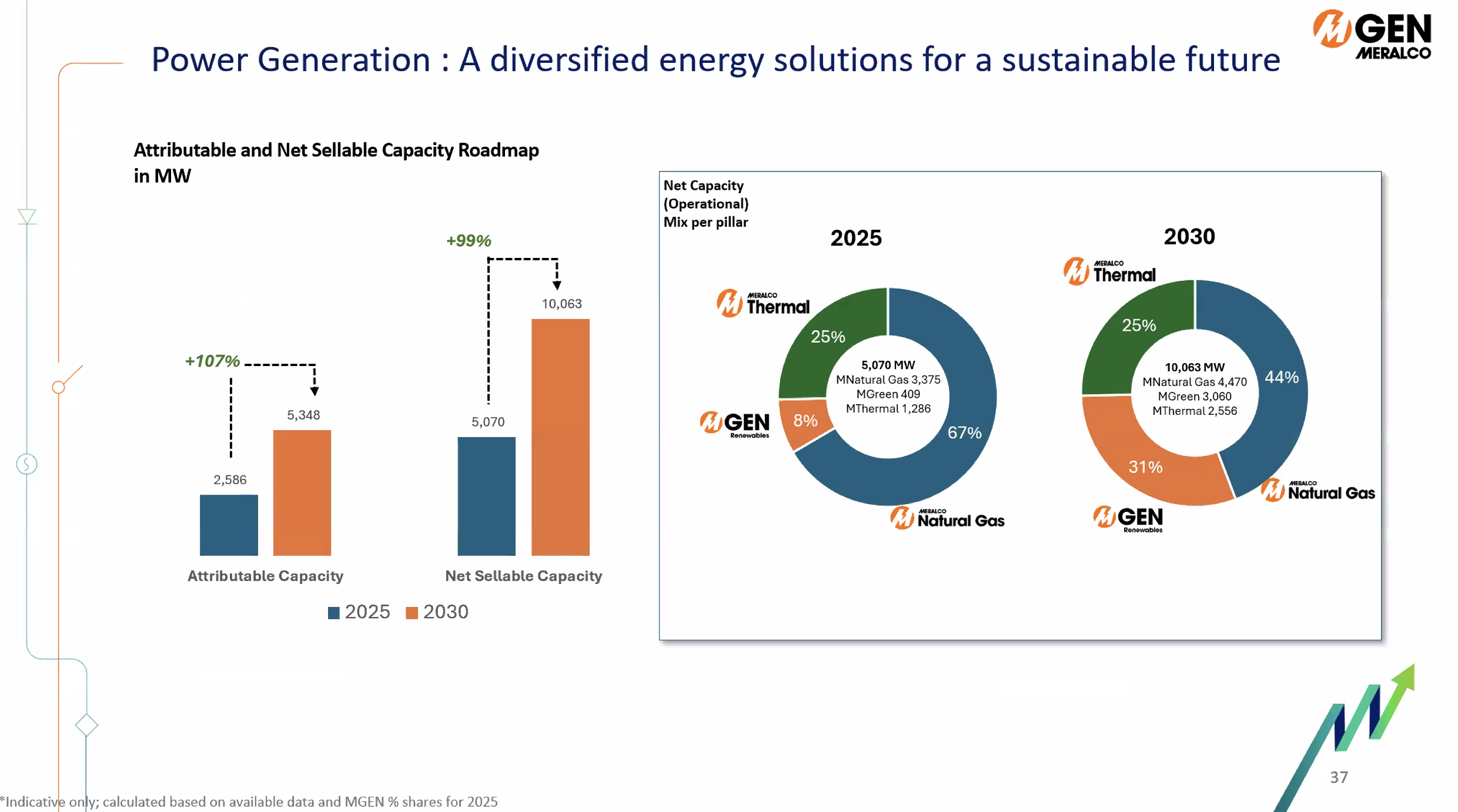

The most consequential expansion was into power generation, carried out through Meralco PowerGen Corporation, known as MGen. What started as a modest equity stake in a handful of plants has grown, through acquisitions and new construction, into a generation portfolio with net saleable capacity of 5,070 megawatts across the Philippines and Singapore, already one of the largest in Southeast Asia, and targeted to reach 10,000 megawatts by 2030.

The portfolio is organized into 3 pillars, each serving a different role in the country’s electricity supply.

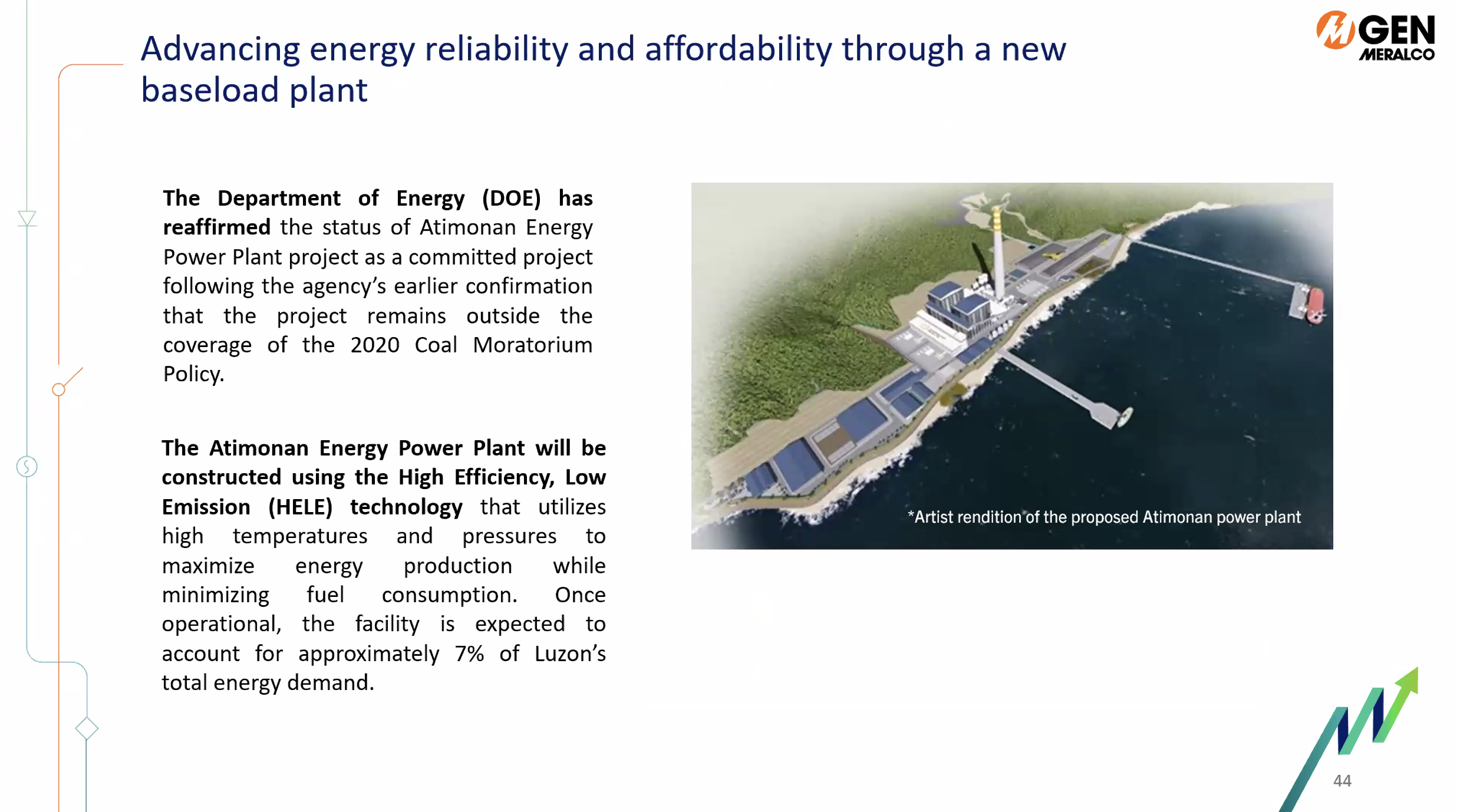

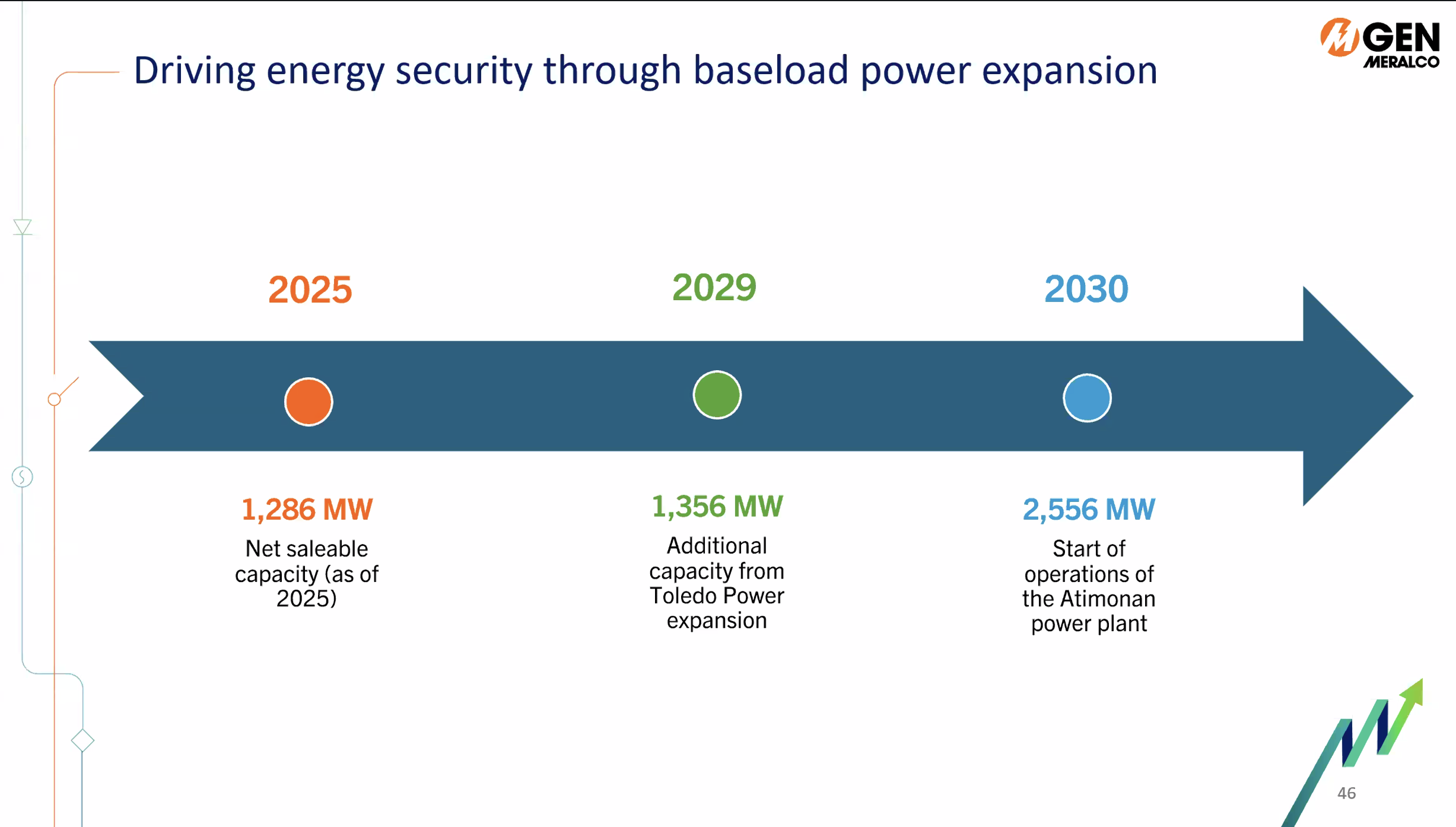

The baseload foundation. MGen’s thermal plants, primarily coal, run between 16 and 18 hours a day, providing the steady, predictable baseline supply that keeps the grid from collapsing during periods of peak demand or when other plants go offline. MGen Thermal currently operates 1,286 megawatts of this baseload capacity, concentrated in Visayas and Mindanao. Coal is not glamorous, and it is not the direction the energy transition is heading, but it is essential for now, because the grid still depends on it. MGen has received government certification for a planned 1,200-megawatt plant in Atimonan, Quezon that clears the existing coal moratorium policy, meaning the regulator has formally recognized it as an approved project despite the general freeze on new coal. The Atimonan plant will use High Efficiency, Low Emission technology, which burns coal at higher temperatures and pressures to maximize output while reducing fuel consumption, and when fully operational is expected to supply roughly 7% of Luzon’s total energy demand.

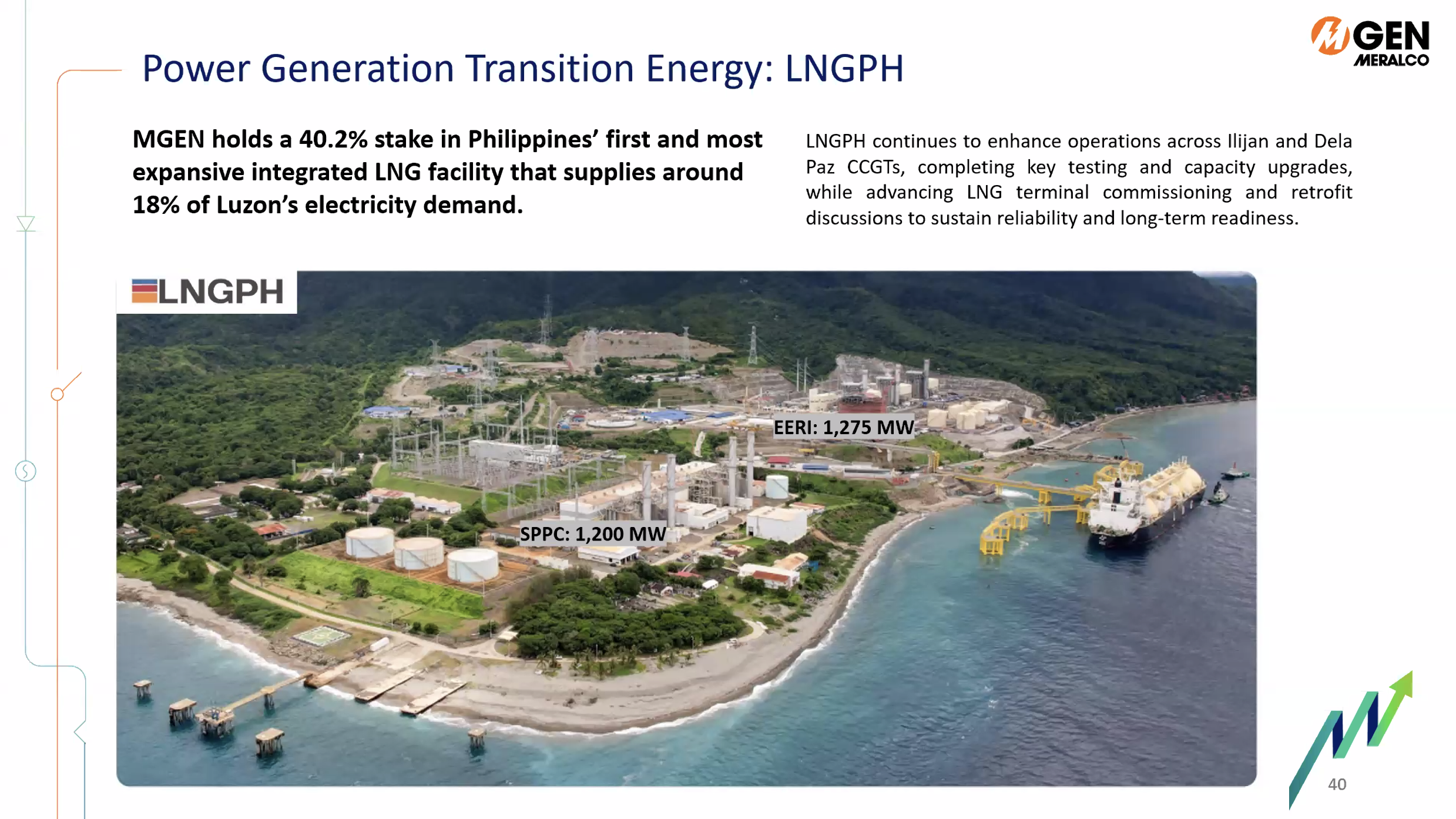

The transition fuel. Natural gas currently makes up 67% of MGen’s total generation portfolio, largely because of a single acquisition made in January 2025. MGen took a 40.2% stake in what is now referred to as LNG PH, an integrated natural gas facility in Batangas that includes 2 gas-fired power plants totaling nearly 2,500 megawatts, plus the country’s first and largest LNG import and regasification terminal. LNG stands for liquefied natural gas, which is natural gas chilled to liquid form so it can be loaded onto tankers and shipped from overseas. The Batangas terminal receives those tanker deliveries, converts the liquid back to gas, and feeds it into the power plants. The facility currently supplies roughly 18% of Luzon’s total electricity demand. In the first quarter of 2026, the LNG PH plants delivered 2,712 gigawatt-hours of energy, 66% higher than the same period the year before, as MGen’s books captured a full 3 months of the operation for the first time after the acquisition.

The gas business also brings a geopolitical exposure that the company addressed candidly during the BPI briefing. LNG prices spiked after the Middle East conflict escalated, rising from pre-war levels of roughly $8 to $12 per MMBTU to highs of $20 to $25, then settling into a range of $16 to $19. As of the time of that briefing, MGen’s fuel supply was secured only through June 2026, with longer-term contracts being negotiated with suppliers in Australia, the United States, Japan, and Russia. An additional on-site storage tank expected to come online in June 2026 would extend the buffer from 15 days of inventory to 20.

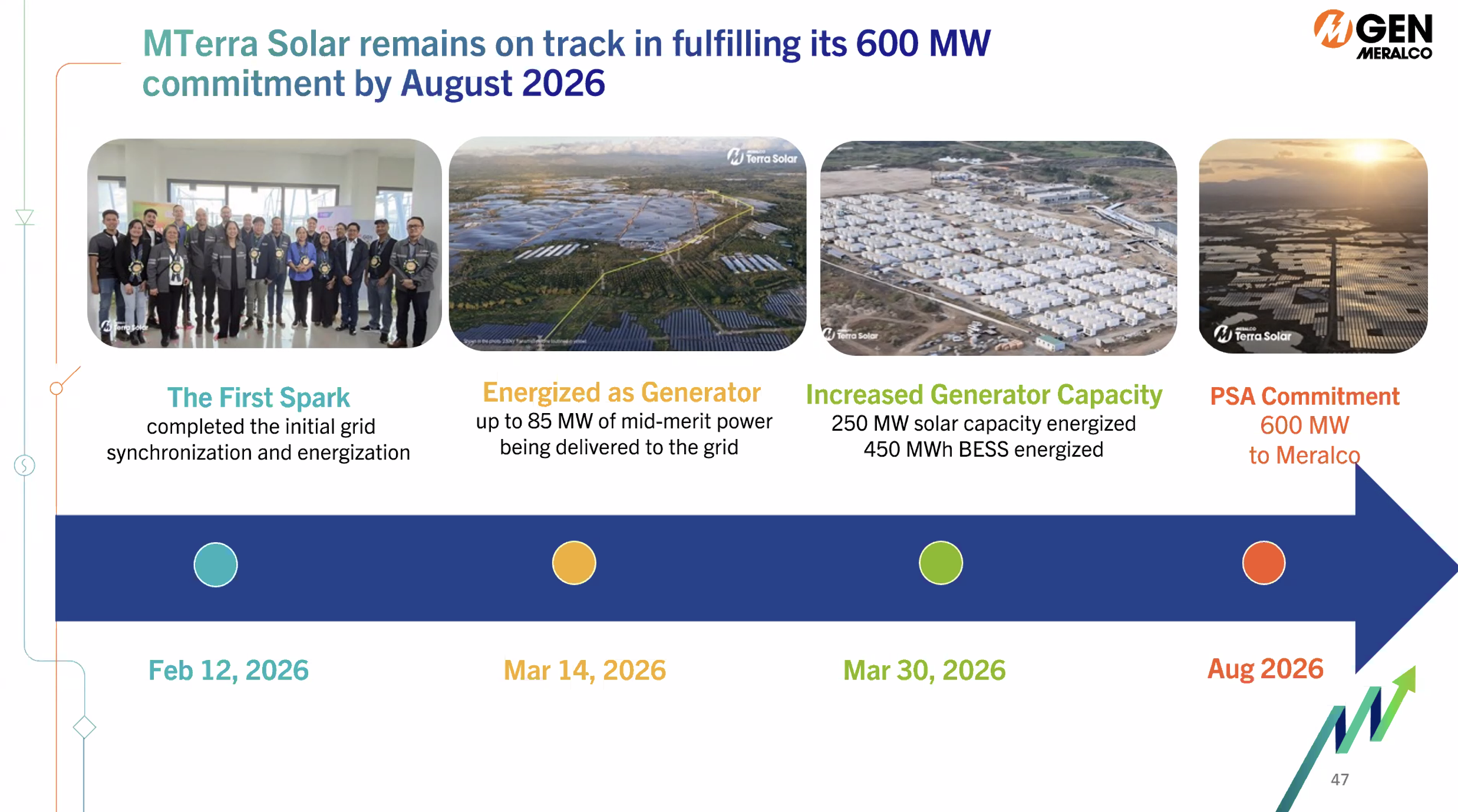

The renewable bet. MGen Renewables currently operates 409 megawatts across 7 solar farms in Luzon, but the number that dominates every conversation about Meralco’s future is the one attached to a single project in Nueva Ecija called MTerra Solar. The project envisions 3,500 megawatts of solar generation capacity paired with 4,500 megawatt-hours of battery storage, a combination that, if completed as designed, would make it the largest integrated solar-and-storage facility in the world.

The battery component is what makes this project unusual and significant. Most solar farms can only generate power when the sun is shining, which creates a supply gap every evening precisely when residential and commercial demand tends to peak. The batteries in MTerra Solar would absorb surplus generation during the day and release it into the grid after sunset, effectively converting an intermittent energy source into something closer to a dispatchable one. Think of it as a giant rechargeable power bank for a significant portion of the Luzon grid.

As of the May 2026 briefing, Phase 1 of MTerra Solar was at 83% construction progress. An initial 85 megawatts had already been energized to the Luzon grid in March 2026, and the project was on track to deliver the full 600 megawatts contracted with Meralco’s own distribution utility by August 2026. Phase 2, covering an additional 250 megawatts, was targeted for early 2027. The project represents an investment of roughly P200 billion and accounted for ~71% of Meralco’s total capital expenditure of P19.5 billion in the first quarter of 2026 alone.

The Singapore foothold. Through an entity called Pacific Light Power, MGen operates gas-fired power plants in Singapore with 830 megawatts of net sellable capacity, and an additional 100 megawatts of fast-track capacity recently brought online. Further expansions of 640 megawatts projected for 2029 and 432 megawatts in a separate plant afterward would grow the Singapore presence considerably. These investments are funded through approximately 1 billion Singapore dollars committed to the market, positioning Meralco as a power producer in one of Southeast Asia’s most sophisticated electricity markets and giving it a template for regional expansion beyond the Philippines.

The longer horizon. MGen signed a feasibility grant of $2.8 million from the US Trade and Development Agency to study the deployment of small modular reactors, compact nuclear plants, as a potential baseload energy source in the Philippines. This is not a nuclear plant announcement. It is a research commitment. But the fact that it is on the table at all illustrates the trajectory: from a regulated wires company in 2001 to a company now seriously studying whether to add nuclear to its generation mix.

The retail electricity business: competing for the customers who can leave

While MGen was expanding into generation, a parallel business was being built on the customer-facing end of the supply chain.

The EPIRA law, in addition to separating the industry into layers, created a category of electricity users who were too large to remain captive Meralco customers. Factories, malls, office towers, data centers, and other large commercial and industrial establishments consuming above a certain threshold were classified as “contestable customers,” meaning they were legally entitled to shop around for their electricity supplier rather than automatically buying from their local distribution utility. This was supposed to inject competition into the supply side of the market.

Meralco’s response was to compete. Through its retail electricity supply arm MPower, the company bids for those large accounts in the open market, offering multi-year supply contracts, green energy options through power purchase agreements, and pricing structures tailored to high-volume buyers. As of early 2026, MPower holds approximately 33% of the contracted demand in the contestable market and 38% of the customer accounts, making it the dominant player in the very market that was designed to let customers escape Meralco.

The structural elegance of this arrangement is worth noting. A contestable customer who signs with MPower has not technically left Meralco. The electricity still travels through Meralco’s wires. The distribution charge still applies. What the customer has done is chosen Meralco’s supply arm over a competitor’s supply arm, while Meralco’s distribution arm continues to deliver the power and collect the wires fee. The customer believes they have exercised a choice. Meralco has simply captured both ends of the transaction.

Rooftop solar and the disruption from below

The expansion into generation and retail supply represents Meralco growing into the parts of the energy chain above and beside it. But a separate challenge is growing from below, and it is one that no corporate strategy can fully neutralize: ordinary customers are increasingly generating their own electricity through rooftop solar panels, and every kilowatt-hour they produce is a kilowatt-hour they do not buy from Meralco.

The scale of this erosion was described candidly during the BPI briefing. In the first quarter of 2026, Meralco estimates it lost approximately 170 gigawatt-hours of sales to rooftop solar installations in its franchise area. That is roughly 1.4% of its quarterly sales volume, and it represents a 40 gigawatt-hour increase from the same period in 2025. The acceleration is being driven partly by geopolitics: as Middle East tensions pushed global fuel prices higher, more Filipino households and businesses looked at their electricity bills and decided the economics of installing solar panels had finally tilted in their favor.

The ratio that best captures Meralco’s predicament here was stated plainly by Ramos during the briefing: for every 5 kilowatt-hours lost to rooftop solar, the company gains back only 1 kilowatt-hour through the growth of electric vehicle charging in its franchise area. It is not a comfortable number.

The response has 2 components.

The first is to become the company that installs and owns the solar panels instead of watching someone else do it. Through MSpectrum, Meralco’s rooftop solar subsidiary, the company offers customers what it describes as a zero-upfront-cost solar solution. Rather than purchasing panels outright, which is how most installations currently happen, a customer signs a contract with MSpectrum, structured like a postpaid mobile phone plan, and pays a fixed monthly subscription or a per-kilowatt-hour rate set 2 to 3 pesos below Meralco’s standard distribution rate. MSpectrum owns and maintains the panels. The customer gets cheaper electricity. Meralco keeps the customer relationship even as that customer partially exits the traditional billing arrangement.

The 2nd component is infrastructure. Meralco is investing P34 billion in the rollout of advanced metering infrastructure, or smart meters, across its franchise area. Currently at 8.2 million customer connections, the company plans to deploy 11 million smart meters over the next decade. Smart meters allow real-time tracking of consumption, enable time-of-use pricing where electricity costs less during off-peak hours, and, most importantly for the longer-term strategy, create the technical foundation for a fully competitive retail market where even ordinary households can eventually choose their electricity supplier. The government’s plan to extend the contestable market down to households consuming as little as 100 kilowatt-hours a month depends entirely on smart meters being in place to track the transactions.

The regional play: why Meralco is thinking beyond the Philippines

The target of doubling MGen’s generation capacity from 5,000 to 10,000 megawatts by 2030 is not simply about serving more of Meralco’s existing customers. Meralco’s distribution franchise area currently needs about 9,000 megawatts at peak demand. A 10,000-megawatt generation portfolio is larger than that. The surplus is intended for wholesale electricity markets, for contestable commercial accounts, and for the ambition of becoming a regional power producer rather than a domestic one.

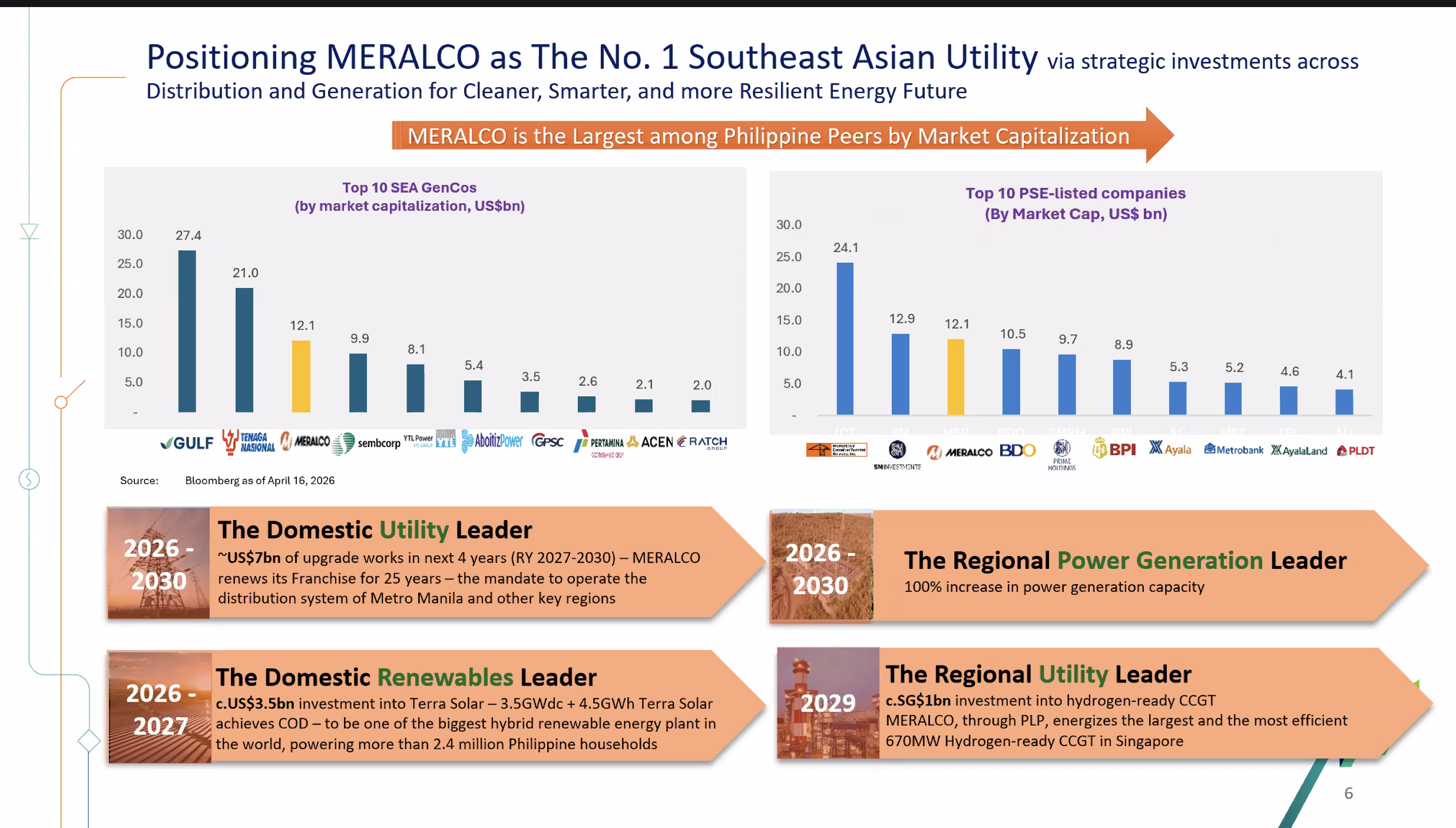

The regional framing is deliberate. At the BPI briefing, Ramos placed Meralco in the company of Gulf Energy of Thailand and Tenaga Nasional of Malaysia when discussing its ranking among Southeast Asian power generation companies by market value, a comparison that would have been unthinkable a decade ago. Its market capitalization as of that briefing was approximately $12.1 billion, having already surpassed SM Prime and BDO, and trailing only ICTSI among the largest publicly listed companies in the Philippines.

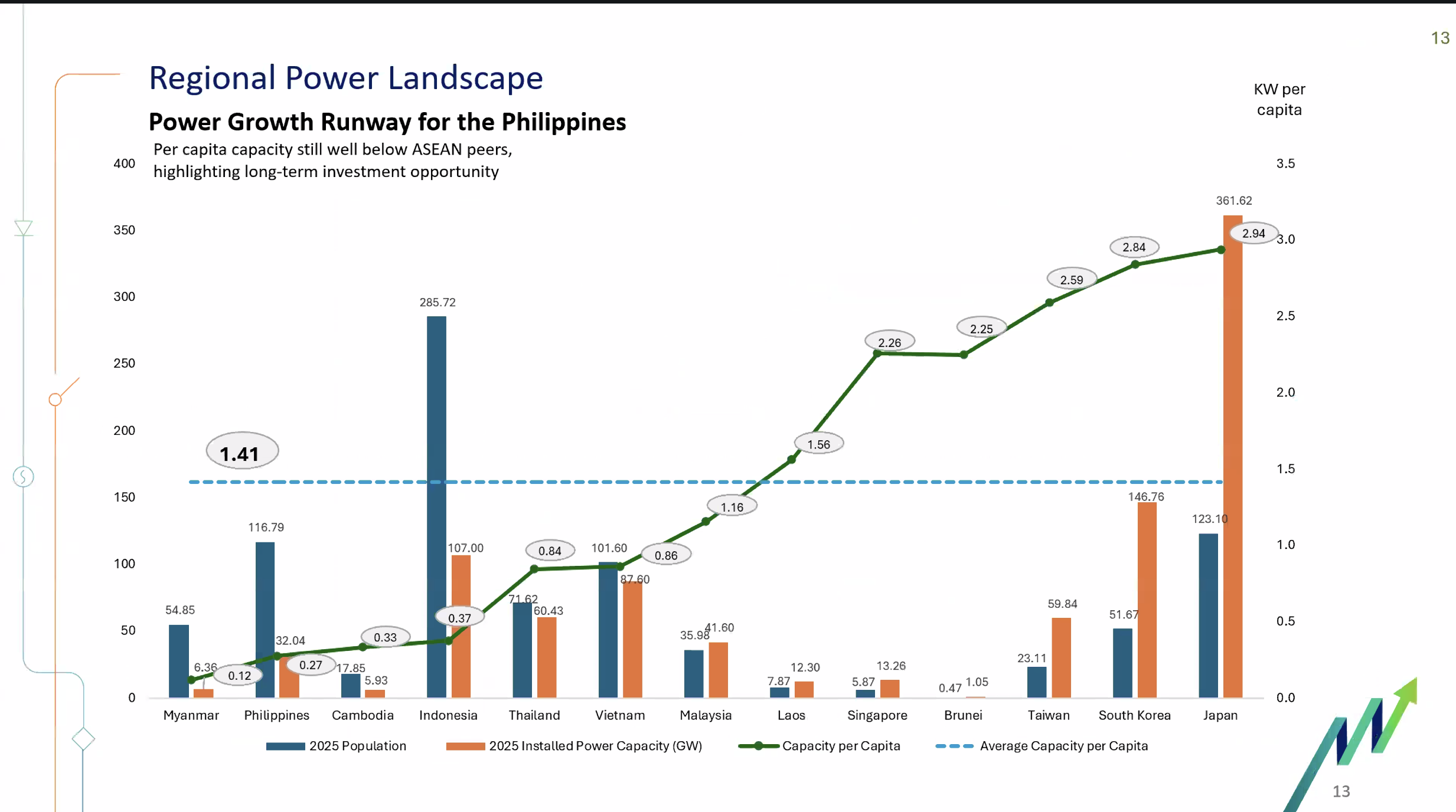

The investment thesis behind the regional play rests on a single data point: the Philippines has some of the lowest installed electricity capacity per capita in Southeast Asia, at 0.27 kilowatts per person against a regional peer group that includes Malaysia, Singapore, Thailand, and Vietnam at substantially higher levels. As the Philippine economy grows and more of the population enters the formal electricity grid, the gap between current capacity and future demand will have to be filled. Meralco, with its growing generation portfolio and its existing relationships across the electricity supply chain, wants to be the company that fills it, not just in Metro Manila, but across Luzon, Visayas, and Mindanao, and increasingly in neighboring markets.

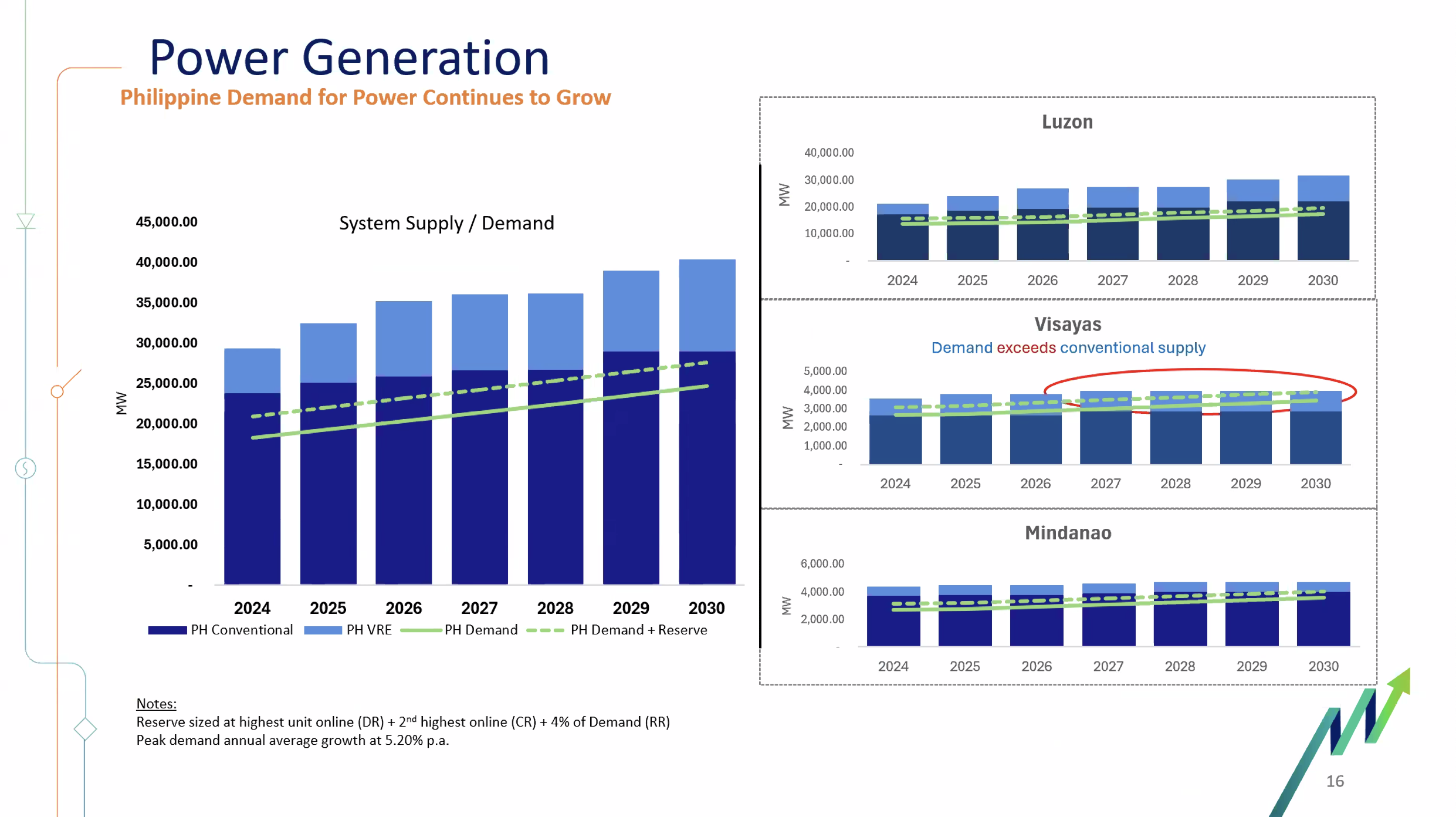

The Philippines’ national power sector has grown at a compound annual rate of 4.7% over the past decade. Meralco’s own energy sales have grown at 4.4% over the same period, slightly below the national average, in part because Visayas and Mindanao have been growing faster. MGen’s expansion into those regions, the Visayas thermal plants, the Toledo battery energy storage facility in Cebu, and the gas plants in Batangas, is partly a response to that arithmetic. If the growth is happening outside Meralco’s distribution franchise area, then the generation business needs to be there to capture it.

The distribution rate reset: the number that will change your bill

Everything described so far, the generation expansion, the retail arm, the rooftop solar play, the regional ambition, belongs to the unregulated side of Meralco’s business. Market rates, competitive dynamics, and the company’s own judgment about risk and return govern those businesses.

The distribution business, which still provides the stable foundation underneath all of it, operates on a different logic entirely. And in 2026, after more than a decade of the distribution rate holding largely flat, that foundation is being renegotiated.

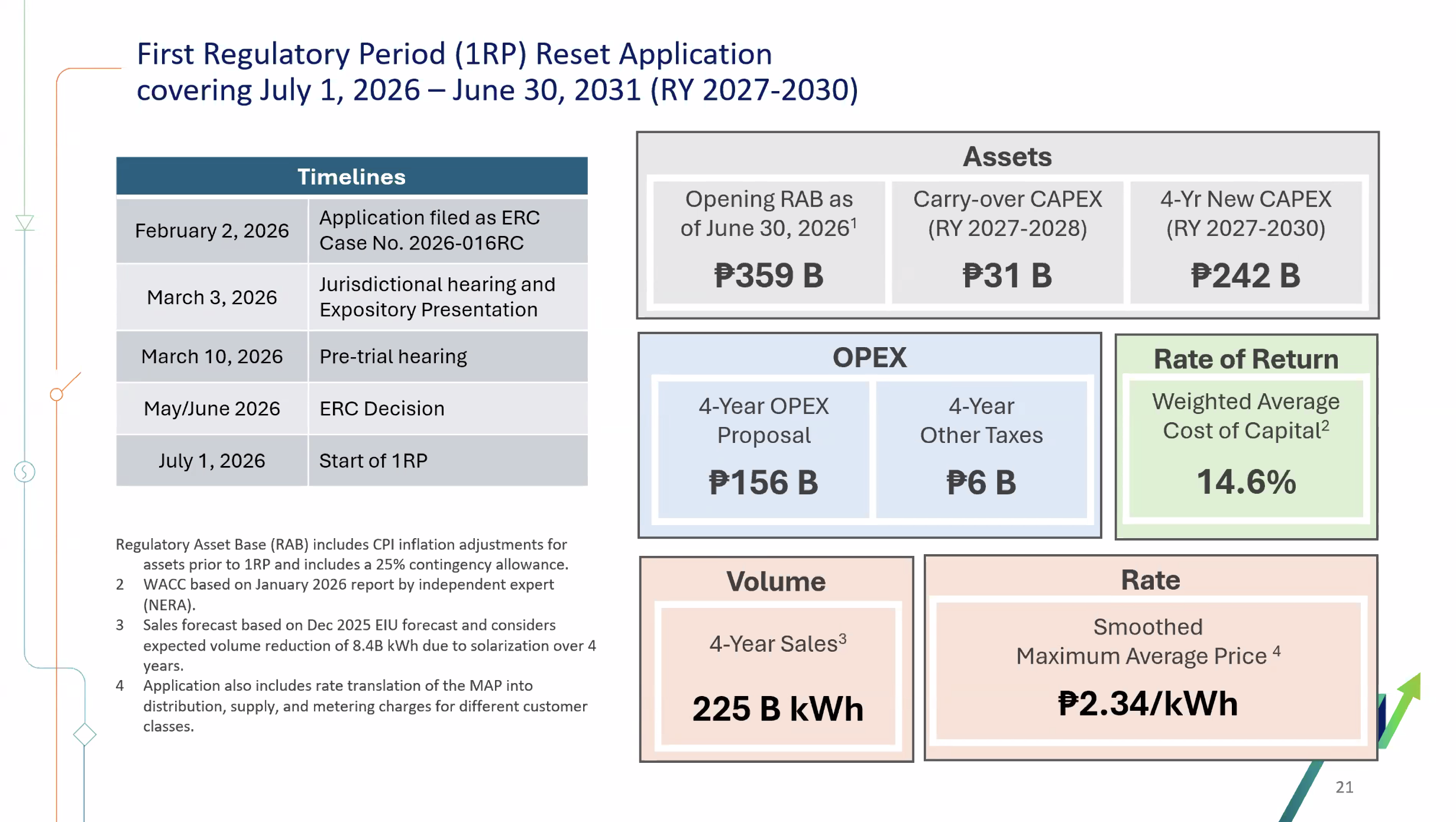

Meralco filed its application for a new distribution rate in February 2026. What it asked for: P2.34 per kilowatt-hour. What it currently charges: P1.35 per kilowatt-hour. The difference, if approved in full, would raise the distribution component of every Filipino’s electricity bill within Meralco’s franchise area by about 70%.

The request is not arbitrary. The formula the ERC uses to set the rate is built on 5 building blocks: the return on capital invested, the return of that capital over time through depreciation, operating and maintenance costs, corporate income tax, and other taxes. The critical input is the “regulatory asset base,” which represents the total value of Meralco’s infrastructure assets, the substations, the cables, the meters, the automation systems. As of the filing date, Meralco’s regulatory asset base was valued at P359 billion. Applied against a weighted average cost of capital of 14.6%, determined by a third-party appraiser, the mathematics of the formula produce a higher allowed revenue than the current rate can deliver.

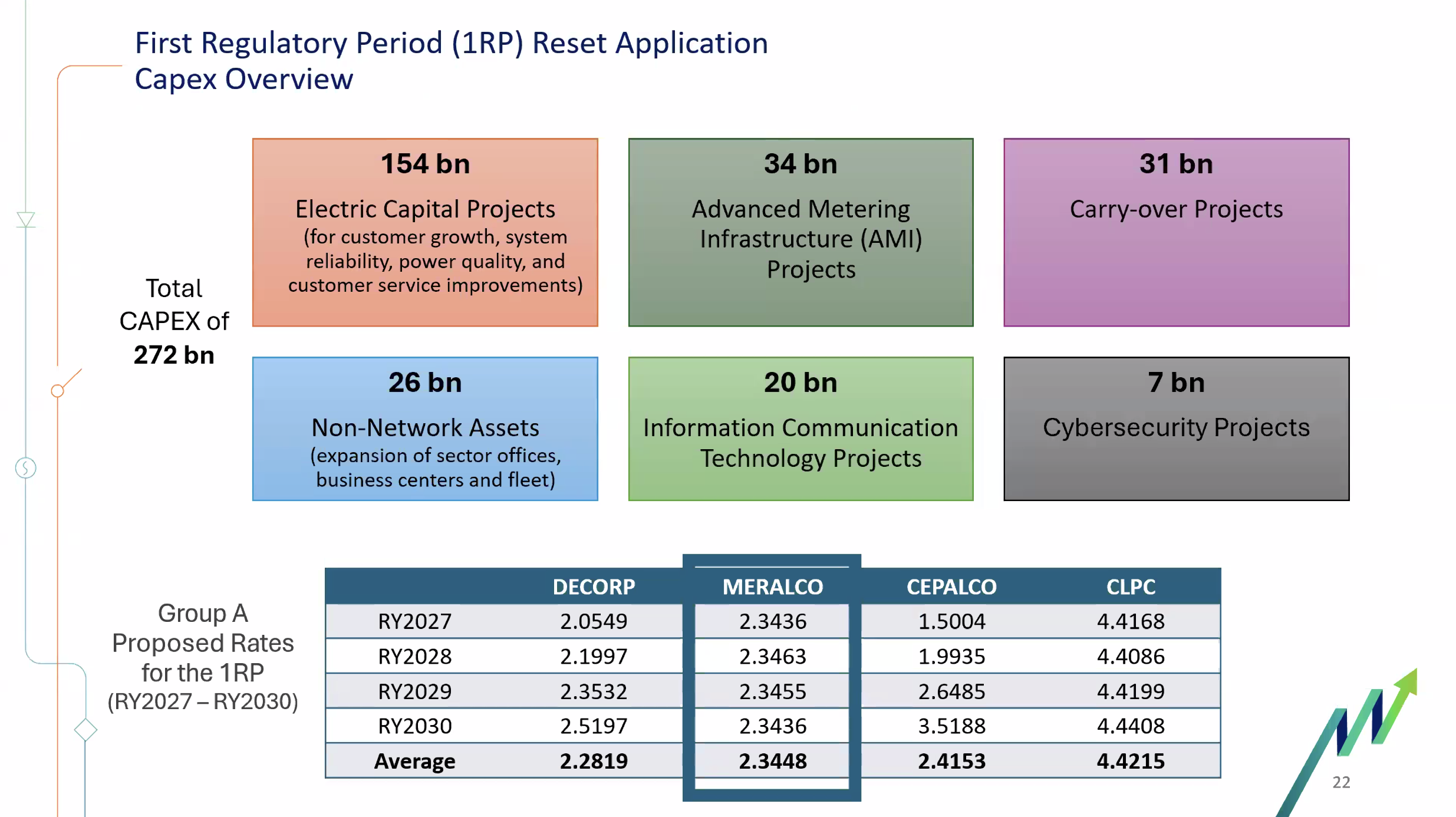

Meralco has also proposed capital expenditure of P242 billion for the 4-year regulatory period covered by the new rate, on top of a P31 billion carryover from prior approved projects. The company has been spending at roughly P40 billion to P45 billion per year on distribution infrastructure since 2023, and it argues that the rate it currently charges has not kept pace with those investments.

Evidentiary hearings took place in April 2026, with Meralco presenting 13 witnesses over 10 days. Interveners filed their witnesses and evidence at the end of April. Clarificatory hearings were running through May. A decision from the ERC was expected by June 2026, with implementation targeted for July 1.

For ordinary Meralco customers, all 8.2 million of them, the outcome of that process is the most direct and immediate consequence of everything described in this piece. The generation business, the Singapore plants, the Terra Solar construction, the retail supply arm, the smart meters: all of it is real and significant and reshaping what Meralco is. But the number that will appear on the bill in July is the one that most Filipinos will actually feel.

The company you will still be paying in 2053

Meralco’s distribution franchise now runs to 2053. Its generation capacity is on track to double in 4 years. It is building what may become the world’s largest solar-and-storage facility. It has power plants in Singapore, a feasibility study for nuclear reactors, a rooftop solar subscription business, a retail electricity supplier, smart meters planned for 11 million customers, an EV charging network under the Movem brand, and a fiber internet service under MeralcoFibr.

In 2021, 86% of its profits came from the regulated business of moving electricity through wires. In the first quarter of 2026, the unregulated businesses have crossed 54% and are still climbing. The company that the 2001 reform law tried to confine to a single lane has, in economic terms, and through subsidiaries and equity stakes and strategic acquisitions, rebuilt something that looks very much like the vertically integrated energy company that EPIRA was designed to prevent, not by defying the law, but by reading it carefully and building in every direction it did not explicitly close.

The delivery driver bought the warehouse, then the trucks, then the factory, and is now studying whether to build a nuclear reactor. The wires into your home are still Meralco’s. What else belongs to them is a list that keeps getting longer.

My 2-part series on Meralco.

- Part 1, The long, complicated life of Meralco, covers the company’s 122-year ownership history, from American tram company to the current Pangilinan-Gokongwei coalition.

- Part 2, From delivery driver to factory owner: How Meralco rewrote its own rules, looks at what the company has become under its current owners — and what it is building toward.

Leave a comment